CORRESP: A correspondence can be sent as a document with another submission type or can be sent as a separate submission.

Published on June 7, 2016

Please reply to:

Direct Tel: 213-542-2121

egelfand@gghslaw.com

June 7, 2016

VIA EDGAR AND FEDEX

United States Securities and Exchange Commission

Division of Corporation Finance

Mail Stop 4628

100 F. Street, N.E.

Washington, D.C. 20549-4561

ATTN: Parhaum J. Hamidi, Attorney-Advisor

| RE: |

QS Energy, Inc. Form 10-K for Fiscal Year Ended December 31, 2014 Response Dated March 15, 2016 Form 10-K for Fiscal Year Ended December 31, 2015 Filed March 15, 2016 Form 10-Q for Fiscal Quarter Ended March 31, 2016 Filed May 10, 2016 File No. 0-29185 |

Dear Mr. Hamidi:

We are submitting this letter on behalf of our client, QS Energy, Inc. (“Company”), in response to the staff’s comment letter of May 27, 2016, concerning the above-referenced filings and the Company’s response letter of March 15, 2016. The staff’s comments and the Company’s responses are as follows:

Staff Comment No. 1:

Form 10-Q for Fiscal Quarter Ended March 31, 2016

1. As applicable, please also give effect to the following comments in your Form 10-Q for the fiscal quarter ended March 31, 2016.

Company Response to Comment No. 1: The Company undertakes to do so.

|

United States Securities and Exchange Commission Division of Corporation Finance |

June 7, 2016 Page 2 |

Staff Comment No. 2:

Form 10-K for Fiscal Year Ended December 31, 2015

2. We note your response to our prior comment 1 and reissue the comment in part. It is unclear from your disclosure which patents that you own are related to your active business. Please expand your disclosure at page 11 to quantify the number of patents which no longer form an active part of your business, and describe any risks to your business that result from any gaps that exist in full patent protection.

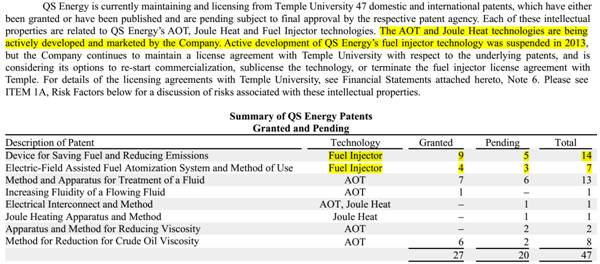

Company Response to Comment No. 2: At page 11 of our 2015 Form 10-K, we identify which patents are no longer part of our active business, stating, “Active development of QS Energy’s fuel injector technology was suspended in 2013, ….” The table which follows that statement identifies 21 patents (13 granted, 8 pending) which are directly related to the fuel injector technology. The following excerpt is from page 11 of our 2015 Form 10-K (emphasis added):

The statement above directs the reader to ITEM 1A, Risk Factors of the Form 10-K for discussion regarding risk factors associated with these patents, where risks related to gaps that may exist in full patent protection are discussed, including the following excerpt from page 18:

At page 7 of our Form 10-Q for the period ended March 31, 2016, we summarize patents as “47 domestic and international patents and patents pending”, but did not provide any further detail. In the following paragraph, readers are advised to read the Form 10-Q in conjunction with our 2015 Form 10-K. In our next Form 10-Q filing (period ending June 30, 2016), we will provide clarification regarding the patents related to active and inactive business activities and specifically direct the reader to the 2015 Form 10-K for patent details. The Form 10-Q specifically directs the reader to ITEM 1A, Risk Factors of the 2015 Form 10-K, where patent risk factors are discussed as detailed above.

We believe the above discussion clarifies and adequately addresses the staff’s comment no. 2. Please advise.

|

United States Securities and Exchange Commission Division of Corporation Finance |

June 7, 2016 Page 3 |

Staff Comment No. 3:

3. We reissue our prior comment 2 in part. You continue to suggest that your AOT technology has been “proven” to “increase the energy efficiency of oil pipeline pump stations.” Based on the information you provided on a supplemental basis and the related disclosures, and for the reasons cited in prior comment 2, please revise your disclosure to remove the claim that the technology has been “proven.”

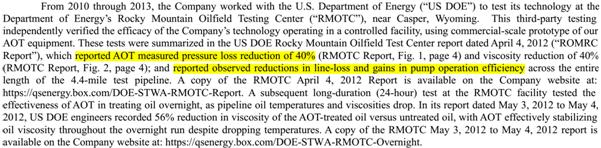

Company Response to Comment No. 3: The full statement referenced in the staff’s comment no. 3, above, is that the “AOT™ has been proven in U.S. Department of Energy tests to increase the energy efficiency of oil pipeline pump stations.” (2015 Form 10-K at pages 3 and F-7). Details of U.S. Department of Energy testing are summarized at page 13 of the 2015 Form 10-K as follows (emphasis added):

This statement provides a link to the full DOE report, specifically drawing attention to Fig. 1, page 4 of the report as follows:

|

United States Securities and Exchange Commission Division of Corporation Finance |

June 7, 2016 Page 4 |

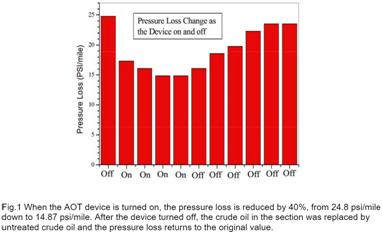

In pipeline operations, reductions in viscosity and pipeline pressure loss directly result in increased pump station efficiency. As noted in the conclusion of the DOE report, “Pipeline line-loss and pump motor power consumption were reduced for a given flow rate during the observed test.” A full copy of the DOE report can be found online at: https://qsenergy.app.box.com/doe-stwa-rmotc-report.

The Form 10-K also provides summary information

on an overnight test run at the DOE facility, which reached the same conclusion. A link to this report, as provided in the Form

10-K is:

https://qsenergy.box.com/DOE-STWA-RMOTC-Overnight.

Although the statement in the 2015 Form 10-K is specifically limited to results proven at the DOE test facility, each subsequent test has yielded similar results further demonstrating that the AOT does improve pump station efficiency. As detailed in the 2015 Form 10-K at page 13:

| · | In its report dated June 26, 2012 (“PetroChina Report”), PetroChina concluded, “The above series of tests

show that it is very effective to use AOT to reduce the viscosity of crude oil. We can see that AOT

has significantly reduced the viscosity of Daqing crude oil, Changqing crude oil, and Venezuela crude oil, and

greatly improved its flow rate.” (PetroChina Report, page 15). A copy of the PetroChina Report is available online

at: https://qsenergy.box.com/PetroChina-STWA-Report |

| · | In its summary report dated February 5, 2015, ATS concluded that i) data indicated a

decrease in viscosity of crude oil flowing through the TransCanada pipeline due to AOT treatment of the crude oil; …

A copy of the ATS summary report dated February 5, 2015 is available on the Company website at: https://qsenergy.box.com/ATS-AOTSummaryRpt A copy of the ATS field test report dated October 6, 2014, with certain confidential information redacted, is available on the Company website at: https://qsenergy.box.com/ATS-AOT-Detailed-Report |

Despite early difficulties experienced with the AOT operating on Kinder Morgan’s condensate pipeline, current testing performed subsequent to the Company’s 2015 Form 10-K filing have resulted in sustained overnight operations and testing. Viscosity measurements collected in the field by QS Energy personnel indicated viscosity reductions consistent with expectations based on laboratory tests performed at Temple University. Pipeline operations data collected by Kinder Morgan personnel showed viscosity reduction and pipeline pressure drop consistent with both laboratory results and in-field measurements collected by QS Energy personnel. These results were summarized in the March 31, 2016 Form 10-Q at page 13 as follows (emphasis added):

We believe the DOE test reports from the RMOTC show AOT increases the energy efficiency of oil pipeline pump stations, and that each subsequent test performed supports this conclusion. However, we are very clear in the Form 10-K and Form 10-Q submissions to point out that the efficacy of the equipment has yet to be proven, and that the benefits provided by AOT may not be sufficient to attract customers, stating on page 16 of our 2015 Form 10-K, “The commercial viability of QS Energy’s technologies remains largely unproven and we may not be able to attract customers.”

To address the staff’s concerns, we will revise our future filings to state that the AOT technology “demonstrates” or “shows” an increase in the energy efficiency of oil pipeline pump stations, rather than stating that the AOT technology “has been proven” to do so. We believe that the use of the word “demonstrates” or “shows” reasonably addresses the staff’s comments in light, and in the context, of the other disclosures discussed above. Please advise.

|

United States Securities and Exchange Commission Division of Corporation Finance |

June 7, 2016 Page 5 |

Staff Comment No. 4:

4. Similarly, please revise to eliminate the suggestion at page 6 that you have “proven” your “ability to build, deliver and operate [your] AOT equipment on a high-volume commercial pipeline” in light of the details you supplied regarding the problems your equipment has encountered and the lack of any substantial commercial usage. As you state at page 10, you “have not proven the commercial viability of this product.”

Company Response to Comment No. 4: The Company did in fact build, deliver and operate its AOT equipment on TransCanada’s Keystone pipeline; and despite significant unexpected challenges working with electrically conductive crude oil condensate, the Company adapted its technology and is now operating on Kinder Morgan’s crude oil condensate pipeline. In addition, we believe it is important to read this statement in context, presented within the “Business Strategy” section of our 2015 Form 10-K as follows (page 6):

The step of operating on the Keystone pipeline was a major milestone for the Company. Strategically, this was a critical moment, and despite the fact we are no longer installed on the Keystone pipeline, this single milestone event opened the door for us at Kinder Morgan and potential other major pipeline operators. All equipment installed on the Keystone pipeline was highly controlled and regulated. All final design specifications, quality controls and inspections were reviewed and approved by TransCanada with great detail and precision. The equipment built and delivered was massive in scale and presented significant logistic challenges. Our equipment operated successfully under normal Keystone Pipeline operating conditions, operations which were observed and reported by ATS Rheosystems, an independent laboratory. The statement in question is preceded on page 5 by a detailed description of our experience and challenges at TransCanada and Kinder Morgan, which states the efficacy of the equipment has not been proven, as in the following statement:

“While more testing is required to establish the efficacy of our AOT technology, we are encouraged by the findings of these field tests performed under commercial operating conditions. We look forward to further development and commercialization of our technology.” (2015 Form 10-K, page 5)

As stated on page 10, we “have not proven the commercial viability of this product.” To get there, we need to have final proof of efficacy, demonstrate financial benefit to the oil pipeline operators, and address other risk factors related to market adoption as detailed on page 16. However, based on our experience with Kinder Morgan and other potential customers, pipeline operators appear to be comfortable with our ability to build, deliver and operate our AOT equipment.

We believe the use of the word “proven,” in the context of the disclosures and discussion above, does not suggest that the AOT technology is, at this time, commercially viable. Nonetheless, to address the staff’s concerns, we will revise future filings by removing the word “proven” and replacing it with the word “demonstrates” or “shows.” Please advise.

|

United States Securities and Exchange Commission Division of Corporation Finance |

June 7, 2016 Page 6 |

The Company acknowledges and confirms the following:

A. The Company is responsible for the adequacy and accuracy of the disclosures in the filing;

B. Staff comments or changes to disclosure in response to staff comments do not foreclose the Commission from taking any action with respect to the filing; and,

C. The Company may not assert comments as a defense in any proceeding initiated by the Commission or any person under the federal securities laws of the United States.

Please contact me if you have any questions or further comments in this matter.

Very truly yours,

Gartenberg Gelfand Hayton LLP

By: /s/ Edward S. Gelfand

Edward S. Gelfand,

as counsel to the Company

The statements and content contained in this letter are true and accurate and adopted by the Company.

QS Energy, Inc.

By: /s/Gregg Bigger

Gregg Bigger, CEO