QS Energy Issues Regional Update: China and Russia

Greggory M. Bigger

CEO and Chairman

QS Energy, Inc.

SANTA BARBARA, CA -- (Marketwired) -- 09/20/16 -- This is the third installment of our, QS Energy (OTCQB: QSEP), reports on the world's most important oil producing regions. We provide these updates to share with investors our insights on today's dynamic global energy markets and to highlight strategic deployment opportunities for our AOT technology in these high-output areas.

Among the world's oil and gas regions none are vaster or more diverse than Eurasia. Home to both the world's largest importer of oil and the top producer of both oil and natural gas, the immense geography and natural resources of the Russian Federation and enormous population and thriving manufacturing sector of the People's Republic of China position this region as one of the industry's most active and pivotal. Due to the unique characteristics of these centrally-controlled and increasingly diplomatically aligned nations, we will separately discuss the vibrant energy markets of Western Europe and Central Europe, and to a lesser degree, Eastern Europe in an upcoming report.

Consisting of 36.2% of the Earth's land mass and roughly 70% of the global population, Eurasia is generally considered to comprise the entirety of the continents of Europe and Asia. Covering a total of approximately 21,000,000 square miles, Eurasia stretches from the Arctic Ocean in the north, to the Mediterranean Sea and Indian Ocean across its southern coastline, and is bounded by the Pacific Ocean on the east and Atlantic Ocean on its western coast. Of the 103 nations that make up the imprecise geographic definition of Eurasia (geopolitical definitions have varied throughout history), China and Russia are by far the largest producers and consumers of energy, ranking among the top five in petroleum, natural gas, coal output, and electricity generation in the world today.

China: Growing Energy Dominance

Until the 1990s China was largely an energy isolationist, reserving most of its impressive coal, petroleum and natural gas production for domestic consumption. Due to its economic reforms of 1978, rapidly growing manufacturing and industrial sectors, and the rise of a consumer class, China began to gradually open its energy industry to foreign involvement, expanding its coal mining, and natural gas and oil extraction. Beginning in the mid-1980s, direct foreign investment and joint ventures were permitted for the first time, helping to improve the operations and competitiveness of China National Petroleum Corporation (CNCP), and China National Petroleum and Chemical Corporation (Sinopec). In addition to more fully exploiting the primary oil fields in the east (Daqing), new projects were launched to tap reserves in the north-west Xinjiang basins (Tarim, Turpan-Hami, Junggar) and to explore the potentially massive offshore (Bohai Bay) deposits through China National Offshore Oil Company (CNOOC Group). More recently, the Liaohe field in the northeast, China's largest heavy oil field which covers 112,800 square miles, has reached an annual output of 5 million tons. Newly developed enhanced oil recovery techniques employed by PetroChina Liaohe Petrochemical Company, a subsidiary of CNPC, such as injecting boiler flue gas in combination with steam, has increased production of Liaohe by as much as 60%.

By 2002 China's annual crude oil production had reached 1,298,000 barrels, making it the third largest non-OPEC producer behind Russia (2,704,000) and the United States (2,098,000). Due to demand outstripping production, by 2014 China was importing roughly 7 million barrels of oil daily, making it the world's second largest consumer of petroleum products after the U.S.

Russia: Massive Reserves Provide Geopolitical Clout

By any measure the former Soviet Union is a major player in the global energy market. Russia has massive coal, natural gas and oil reserves, both in production and undiscovered. The U.S. Geological Survey estimates that this 6.6 million square mile nation, the world's largest, has the planet's highest volume of undiscovered deposits of natural gas (estimated at 6.7 trillion cubic meters) and some 22 billion barrels of oil, second only to the probable reserves of Iraq.

Although oil and natural gas production began in the late 1800s, output was modest until the then-ruling Romanov Monarchy solicited foreign investment and know-how to develop the Baku oil fields in Azerbaijan and the Volga-Ural Basin. Later, the oil sector helped shape the events which led to the Russian Revolution of 1917. In 1918 Bolshevik agitators drummed up support of the organized workers of the oil and gas industries and eventually set the Baku oil fields afire in response to a political crackdown. The modern age of massive Russian energy production and efficient delivery to market did not begin in earnest until after World War II. Centralized control and poor worker's wages enabled Moscow to undercut oil from the Middle East by half, creating a strong hold on market share and resultant economic influence over its satellite nations. By the 1960s the Soviet Union had re-established its position as the second largest producer in the world, a standing that today alternates between Russia, Saudi Arabia and the U.S.

With its economy largely dependent on energy exports and supplying half of the government's annual budget, Russia has long used its influence as top-tier producer for geopolitical gain and leverage in its relations with the West. In addition to supplying a third of Europe's oil and gas needs Moscow has increasingly become an important supplier to East Asian markets. Recently, Vladimir Putin has strengthened his alliance with Beijing, building a crude oil pipeline traversing the China-Russia border with a second under construction. In April of this year, China's imports of Russian oil hit an all-time high of 33,670,000 barrels, up 52.4% from the year before.

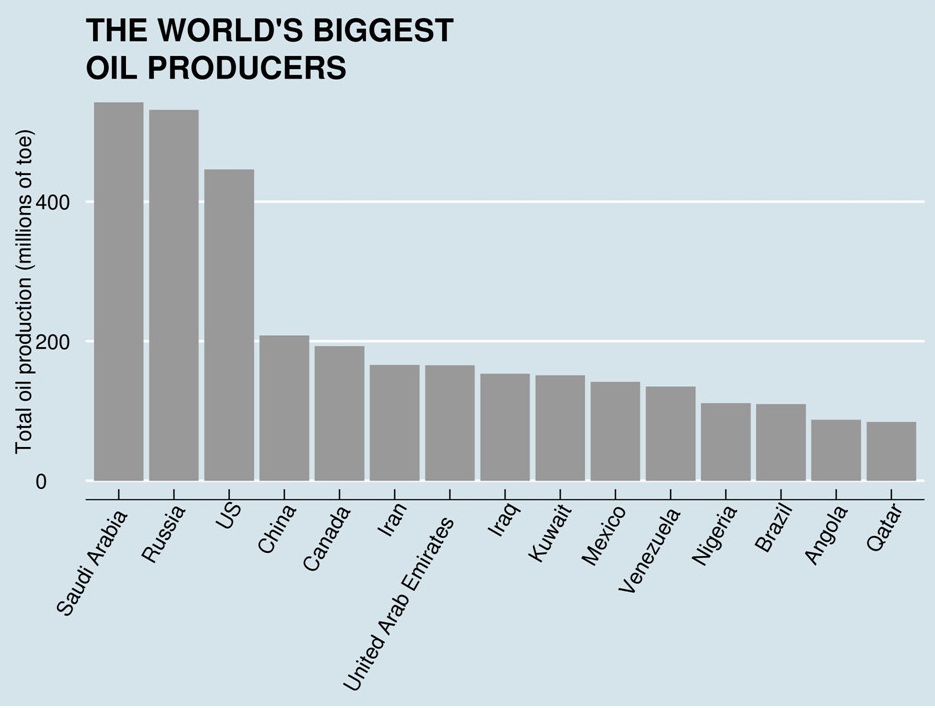

By publicizing the benefits of pipeline flow improvement possible through the use of electrorheology and its ability to effect predictable viscosity reduction, QS Energy has succeeded in entering into non-disclosure agreements with entities in both Russia and China and with producers and transporters in many of the world’s leading oil producing nations. Chart courtesy of BP p.l.c.

AOT Infrastructure Optimization Opportunities

China: Fast-paced economic growth and the dramatic shift from a rural agrarian population to a sprawling, city-dwelling middle class has transformed China into the world's largest consumer of energy. As has occurred in other centrally-controlled communist and socialist nations, reforms have been instituted to move the oil, gas, coal, and hydropower sectors increasingly toward a free market approach to encourage greater efficiencies and competition.

However, despite policies to loosen foreign investment restrictions, China's energy sector continues to be centered around a handful of state-owned entities. The two largest, China Petroleum and Chemical Corporation, also known as Sinopec, and China National Petroleum Corporation (CNPC), parent company of PetroChina, are both vertically-integrated oil and gas producers, refiners, and retailers with E&P activities and operations throughout the world. In 2014 Sinopec produced roughly 360 million barrels of crude oil and 20 billion cubic meters of natural gas, ranking it second only to PetroChina. Indicative of the competitive nature of China's energy sector, in May of this year the China National Audit Office found that several subsidiaries of the Sinopec Group had inflated actual earnings by $3.04 billion through falsified fuel sales.

With the bulk of its oil and gas activities conducted through subsidiary PetroChina, CNPC has remained China's largest energy entity, producing close to 1.2 billion barrels of crude oil and 114 cubic meters of natural gas in 2014, earning revenues of $425 billion. As of last year its 4.4 million barrels of daily output placed it 5th in the world behind Saudi Aramco, Gazprom (Russia), NIOC (Iran) and ExxonMobil. China's other principle crude oil producer is China National Offshore Oil Corporation (CNOOC), an international offshore exploration and production entity.

As of last year China ranked fifth among the world largest oil producers with daily production of roughly 3.89 million barrels, its lowest output since 2003. Downward pressure on spot prices are causing reduced output at some of China’s aging oil fields which analysts expect may continue until Brent Crude levels bounce back and the economics of operating upstream and midstream infrastructure are improved. Map courtesy of the Carnegie Endowment for International Peace, ‘China’s Oil Future’, May, 2014.

As is the case in many hydrocarbon-rich nations, Beijing leadership and energy company executives have wrestled with an inadequate pipeline infrastructure and resultant takeaway challenges. China's largest hydrocarbon basins are the Daqing Field located in the northeast in Heilongjiang province and the Changqing oil field, also to the north, inside Inner Mongolia, an autonomous region. Both have historically produced as much as 280 to 300 million barrels of crude oil annually, output which must be moved thousands of miles inland to the south and west.

Working through QS Energy's strategic partner in China, a variety of government agencies and the leadership at PetroChina have explored the potential for AOT to improve flow and mitigate pipeline capacity limitations. Following the installation in 2012 of an AOT prototype on a closed-loop line and active commercial pipeline in the Daqing Oilfield, an official report was produced by the China Petroleum Pipeline Bureau (CPP), PetroChina, and the PetroChina Pipeline R&D Center. In addition to citing AOT's efficacy in successfully demonstrating "a breakthrough in crude oil viscosity reduction", tests conducted by PetroChina with Daqing crude oil showed significant viscosity reduction and flow rate improvement. More recently, in response to the weakening of global spot prices earlier this year, discussions between our strategic partner in Beijing and top tiered oil transportation companies have resumed with the goal of identifying deployment opportunities within China's fast growing, highly innovative energy sector. At the beginning of this month, a confidential Applied Oil Technology White Paper containing updated information about the value engineered AOT hardware and a detailed cost/benefit analysis was translated into Mandarin for distribution to officials at China's principle crude oil production and transportation entities.

Russia: The evolution and growth of the Russian energy sector has many parallels with China, with the exception that it has perhaps more frequently suffered from inadequate capitalization and the effects of bureaucracy and political in-fighting. Russia's largest, longest operating and biggest publicly traded oil company is Rosneft. Formed in 1933 with assets culled from the former Soviet Union's Ministry of Oil and Gas, Rosneft's operations were later spun off to create ten, separate but integrated energy companies. Beginning in 2004 Rosneft grew dramatically through the acquisition of assets of Yukos, a once-dominant E&P company controlled by oligarch Mikhail Khodorkovsky. Throughout the 2000s further assets were acquired and a 2006 IPO provided $10.7 billion in capital and a market valuation of $79.8 billion. In 2011, joint development projects with ExxonMobil were announced to share the output of fields on Russia's Arctic shelf, a partnership that has grown to include Rosneft participation in projects in Texas and the Gulf of Mexico.

One of Russia's most profitable and international oil companies is Lukoil, a publicly traded corporation formed in the 1991 merger of three state-run Siberian entities. Based on the western model of operating as a fully integrated company active in E&P, refining and distribution/retailing, Lukoil has largely avoided the problems that have often hamstrung Russia's energy sector and today has operations in over 30 regions worldwide with revenues of over $114 billion. In 2013 Lukoil purchased Samara-Nafta, Hess Corporation's Russian operations for $2 billion. Due to its revenues and private sector status, Lukoil is possibly the Federation's largest taxpayer with liabilities of approximately $30 billion annually.

Since the privatization of the Russian oil industry began in 1999 production has soared to just under 10 million barrels per day, positioning it as the world’s second largest exporter with $86.2 billion in 2015 exports, just behind Saudi Arabia ($133.3 billion). Map courtesy of Transneft.

With immense oil reserves straddling seven time zones and over 5,700 miles from west to east, its perhaps not surprising that Russia is home to the world's largest oil pipeline company. Headquartered in Moscow and fully state owned, Transneft moves roughly 90% of all oil produced in Russia through 43,400 miles of pipeline. As the entity responsible for transporting crude oil to refineries, truck and rail facilities, and ports for exporting to foreign markets, Transneft's trunk pipelines are supplied by many hundreds of feeder lines originating from each of the country's primary production regions. Among Russia's largest oil deposits are the North Caucus and Caspian Sea in the west, the Ural-Volga basin, Timan-Pecora and Western Siberia deposits in central Russia, and Eastern Siberia and northern Krasnoyarsk Krai fields in the east.

Following an extensive, multi-year review of potential deployment locations for AOT systems, we have sent representatives to give initial presentations to the leadership of some of Russia's principle crude oil producers and transporters. Our immediate goal is to secure a variety of 4-gallon oil samples from the largest basins for testing by Temple University. With sufficient viscosity reduction data and metrics concerning pipeline characteristics we expect to produce detailed hydraulic analysis output to predict the potential of AOT to improve the flow of Russia's heavy and super heavy crude on key portions of their over 70,000 miles of pipeline infrastructure. At the request of the government and industry officials QS Energy representatives have translated a confidential Applied Oil Technology White Paper into Russian and submitted them to several Russian oil transportation companies for further review and consideration.

In our next Regional Update, we will discuss the Western Europe and Scandinavian oil producing regions and provide an update on our collaborative efforts to adapt AOT technology to subsea infrastructure in the North Sea and other offshore applications.

We invite you to contact us anytime with your questions, comments or suggestions at investor@QSEnergy.com or sales@QSEnergy.com. For QS Energy news and articles concerning the energy industry, follow us on Twitter and LinkedIn.

For further information about QS Energy please read our SEC filings at www.sec.gov, and, in particular, the risk factor sections of those filings.

Safe Harbor Statement:

Some of the statements in this release may constitute forward-looking statements under federal securities laws. Please visit the following link for our complete cautionary forward-looking statement: http://www.qsenergy.com/site-info/disclaimer.

Sincerely,

Greggory M. Bigger

CEO & Chairman

QS Energy, Inc.

Disclaimer

All statements and expressions are the sole opinion of the company and are subject to change without notice. The Company is not liable for any investment decisions by its readers or subscribers. It is strongly recommended that any purchase or sale decision be discussed with a financial advisor, or a broker-dealer, or a member of any financial regulatory bodies. The information contained herein has been provided as an information service only. The accuracy or completeness of the information is not warranted and is only as reliable as the sources from which it was obtained. Investors are cautioned that they may lose all or a portion of their investment in this or any other company.

Information contained herein contains "forward looking statements" within the meaning of Section 27A of the Securities Act of 1933, as amended and Section 21E of the Securities and Exchange Act of 1934, as amended. Any statements that express or involve discussions with respect to predictions, expectations, beliefs, plans, projections, objectives, goals, assumptions or future events or performance are not statements of historical facts and may be "forward looking statements". Forward looking statements are based on expectations, estimates and projections at the time the statements are made that involve a number of risks and uncertainties which could cause actual results or events to differ materially from those presently anticipated. Forward looking statements may be identified through the use of words such as "expects", "will", "anticipates", "estimates", "believes", or by statements indicating certain actions "may", "could", "should" or "might" occur.

Company Contact

QS Energy, Inc.

Tel: +1 805 845-3581

E-mail: investor@QSEnergy.com

Investor Relations

QS Energy, Inc.

Tel: +1 805 845-3581

E-mail: investor@QSEnergy.com

Source: QS Energy, Inc.

Released September 20, 2016